A look back at 2025

The year 2025 was the third warmest on record, with the three-year average temperature for 2023–2025 reaching 1.48°C above pre-industrial levels (World Meteorological Organization, WMO). In Japan, temperatures exceeded 40°C at multiple locations during the summer, and the number of people hospitalized due to heatstroke surpassed 100,000—the highest since records began in 2008. There were frequent reports of linear rainbands (successive, stationary bands of intense rainfall), and a range of weather events vividly demonstrated the growing severity of climate change. Extreme weather also had major impacts on agriculture and fisheries.

Internationally, since taking office in January 2025, U.S. President Donald Trump has denied climate science and systematically dismantled decarbonization efforts—disbanding relevant government bodies, rolling back support for renewable energy, disengaging from UN-led climate agreements and processes, and reviving the fossil fuel industry. These developments have contributed to a slowdown in global decarbonization efforts. At the same time, ongoing conflicts such as those in Ukraine and Gaza have deepened global instability, making it difficult to foresee progress on climate action.

In Japan, the government adopted the Global Warming Countermeasures Plan, which sets greenhouse gas (GHG) emission reduction targets (NDC) (60% by FY2035 and 73% by FY2040 compared to FY2013), along with the 7th Strategic Energy Plan, which defines energy policy through 2040. While the energy plan aims to increase renewables to 40–50% of the electricity mix by 2040, it still envisions 30–40% from thermal power (combustion) and around 20% from nuclear, largely maintaining the current energy policy. Meanwhile, in response to rising energy prices, the government implemented substantial support for fossil fuel consumption, including subsidies for electricity and gas, and the removal of the provisional gasoline tax rate. Efforts to accelerate renewable energy deployment have themselves stalled amid weakening momentum, and climate policy has faded from focus despite growing public concern.

Outlook for 2026

In 2026, U.S. President Trump is likely to continue exerting a strong influence on global affairs, though the extent and nature of the impact are difficult to foresee. Japan is expected to support gas-fired power development and next-generation nuclear technologies as part of cooperation with the United States, raising concerns that Japanese companies’ decarbonization efforts may regress in line with the U.S. shift back toward fossil fuels. This underscores the need to make decisions from a medium- to long-term perspecitive that takes into account the risk of such investments becoming stranded assets. Geopolitical developments, including the situation in Iran, also add uncertainty to fossil fuel prices. Given Japan’s high dependence on fossil fuels and vulnerability in times of crisis, this presents an opportunity to reaffirm the importance of expanding renewable energy as a secure domestic energy source.

Japan’s emissions trading system (GX-ETS) launches in April. Covered companies will move to a mandatory system from a voluntary efforts system in which CO₂ emissions kept within government-allocated allowances. Meanwhile, even as moves emerge to restrict environmentally destructive large-scale solar developments, policy support for renewable energy remains weak. In 2026, it is hoped that renewable energy projects—including offshore wind—will regain momentum and move forward more rapidly.

Across the country, extreme heat and climate-related disasters are expected. To minimize impacts and strengthen energy independency, it will be increasingly important to implement a wide range of adaptation measures, while also improving building standards, energy efficiency, and renewable energy deployment to enhance local resilience.

Commentary

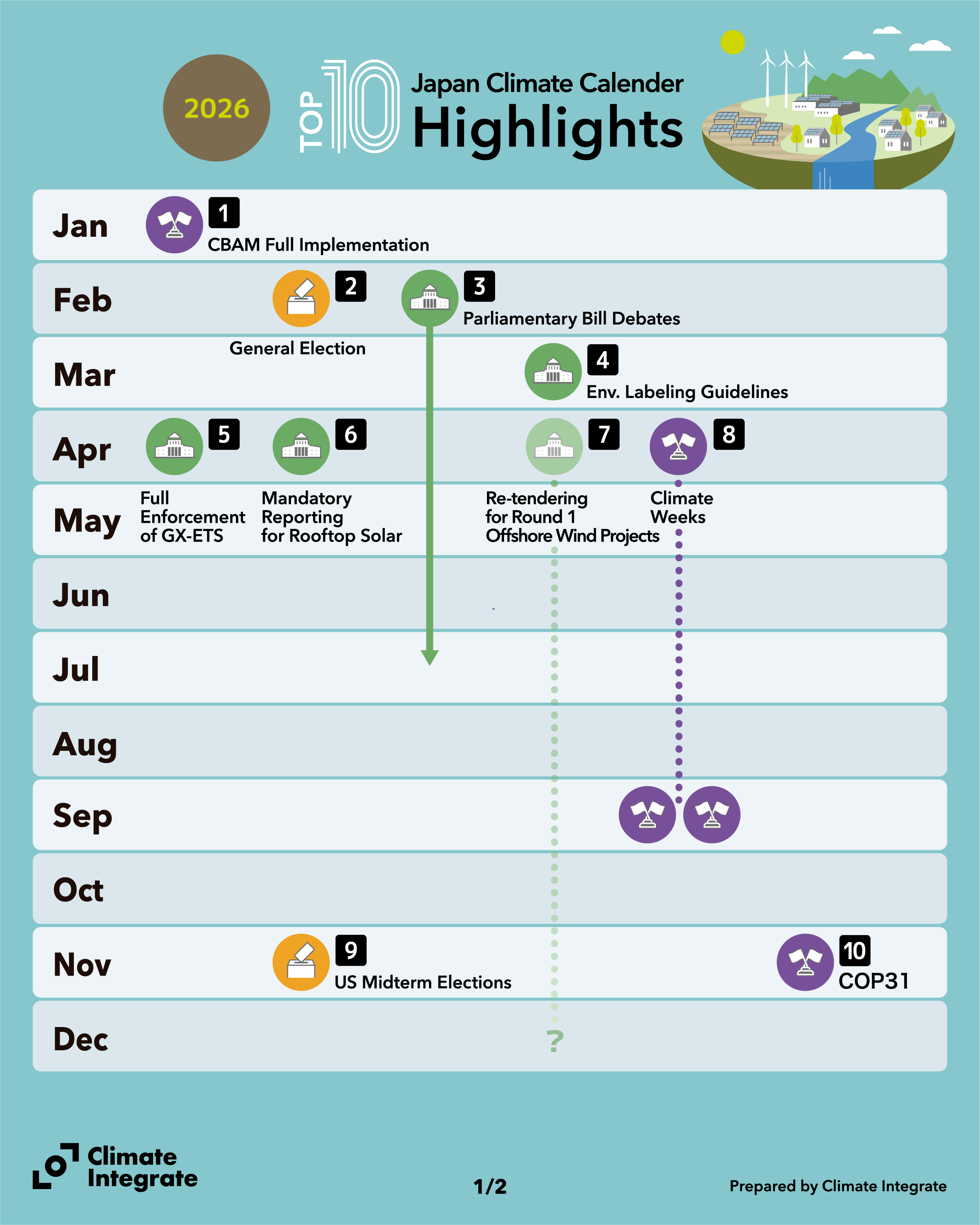

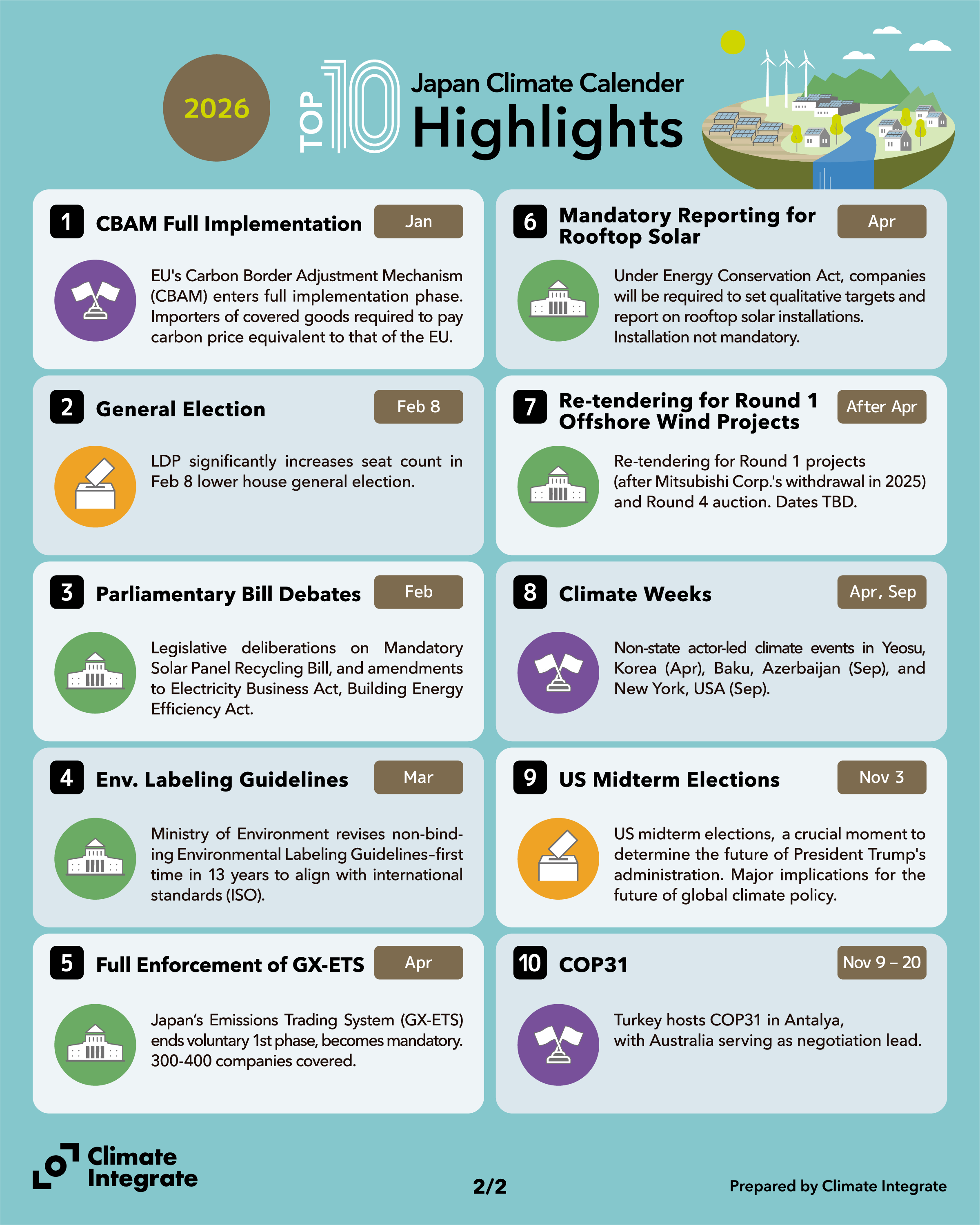

1. CBAM Full Implementation (Jan)

The European Union (EU) has begun full implementation of the Carbon Border Adjustment Mechanism (CBAM). Importers are required to pay a carbon price equivalent to that applied within the EU. The initial scope covers six sectors: steel, aluminum, cement, fertilizers, electricity, and hydrogen. Importers must purchase and surrender CBAM certificates corresponding to embedded emissions. While the immediate impact on Japan is limited, it could grow significantly as the scope expands. Japan’s emissions trading system (GX-ETS), launching in April, introduces carbon pricing, but given that carbon prices in Japan are significantly lower than under the EU ETS, additional payments through CBAM may be required.

2. General Election (Feb 8)

On January 23, the first day of the Diet session, Prime Minister Sanae Takaichi announced the dissolution of the House of Representatives, triggering a general election. In the February 8 vote, the Liberal Democratic Party (LDP) significantly increased its seats to 316, comfortably surpassing the majority threshold (233). Campaign debates focused primarily on immediate concerns such as inflation and tax cuts, with little attention given to climate change. While the Takaichi administration continues existing climate policy directions, their priority remains very low, making it necessary to monitor progress under the Global Warming Countermeasures Plan and Strategic Energy Plan.

3. Parliamentary Bill Debates (Feb–Jul)

During the 221st Diet session in 2026, several bills are expected to be introduced, including legislation on solar panel recycling, amendments to the Electricity Business Act, and revisions to the Building Energy Efficiency Act.

• Mandatory Solar Panel Recycling (Ministry of the Environment)

A legal framework is expected to be established for recycling solar panels, large volumes of which are projected to be discarded from the 2030s onward. Originally scheduled for submission in 2025, the bill was postponed due to disagreements with the Cabinet Legislation Bureau over cost allocation. The revised approach shifts responsibility from manufacturers to power producers and installers that generate large volumes of solar panel waste. Strengthening recycling and reuse is essential for expanding solar power deployment.

• Amendments to the Electricity Business Act (METI)

A new system is planned by METI (Ministry of Economy, Trade and Industry) to provide government financing for large-scale, long-term power generation and grid investments that are difficult to fund privately. The Organization for Cross-regional Coordination of Transmission Operators (OCCTO) is expected to take this role alongside financing support for the development of interregional transmission lines. Eligible power generation projects will be facilities with capacities of 500 MW or more, mainly nuclear and large-scale thermal power plants. OCCTO is expected to finance part of the costs of constructing or upgrading such facilities, with government-backed debt guarantees also anticipated. Critics argue that this mechanism would run counter to the transition toward renewable energy.

• Amendments to the Building Energy Efficiency Act (MLIT)

Amendments to this Act by MLIT (Ministry of Land, Infrastructure, Transport and Tourism) are planned with the aim of reducing CO₂ emissions across the lifecycle of buildings—referred to as lifecycle carbon (LCCO₂), encompassing emissions from materials production through construction to demolition—through the implementation of lifecycle assessment (LCA). The government intends to establish systems for calculating and evaluating LCCO₂ and to require building owners of large-scale projects to submit reports. The objective is to reduce the environmental impact of buildings, including Scope 3 emissions.

4. Environmental Labeling Guidelines (Mar)

For the first time in 13 years, the Ministry of the Environment will revise its environmental labeling guidelines under the Act against Unjustifiable Premiums and Misleading Representations. Aligned with international standards (ISO), the revised guidelines aim to prevent “greenwashing” by setting out five core requirements:

- Avoid vague or misleading environmental claims

- Provide explanatory information for claims

- Ensure data and methodologies used for verification are available

- Base comparative claims on appropriate LCA assessments and data

- Ensure accessibility of information for evaluation and verification

The guidelines, however, are not legally binding.

5. Full Enforcement of GX-ETS (Apr)

With its voluntary first phase ending, Japan’s emissions trading system (GX-ETS) will become mandatory in April. About 300–400 companies will be covered (primarily power utilities and energy-intensive industries with Scope 1 emissions exceeding 100,000 tons). Large companies will move from voluntary efforts to a system in which CO₂ emissions must be kept within government-allocated allowances. Whether the system is designed and operated in line with Japan’s NDC will be a key determinant of its effectiveness.

6. Round 1 (Re-tender) and Round 4 (New Auction) for Offshore Wind (TBD)

Following Mitsubishi Corporation’s withdrawal from offshore wind projects in 2025, the government plans to re-tender Round 1 projects and proceed with Round 4 auctions, though timing remains unclear. The 6th Strategic Energy Plan sets a target of 5.7 GW of offshore wind capacity in operation by FY2030, but delays have emerged due to project withdrawals. Improving the business environment will be critical to restoring momentum.

7. Mandatory Reporting for Rooftop Solar (Apr)

The Energy Conservation Act currently requires businesses to report on their electricity and fuel use through regular reporting obligations. From April, it will introduce requirements for businesses to set qualitative targets and report on the installation of rooftop solar systems. However, the requirement applies to reporting only, and there is no obligation to install solar power systems.

8. Climate Weeks (Apr, Sep)

A combination of factors—including the United States’ declaration of withdrawal from the UN Framework Convention on Climate Change (UNFCCC) and the Paris Agreement—has led to a decline in international momentum on climate action. However, initiatives led by regions and non-state actors remain vibrant, and the overall trend toward decarbonization continues to advance steadily. A series of events led by non-state actors are scheduled to take place in Yeosu, Republic of Korea (April), Baku, Azerbaijan (September), and New York, United States (September). These developments are expected to build momentum toward COP31 in November.

9. U.S. Midterm Elections (Nov 3)

Midterm elections for both chambers of the U.S. Congress are scheduled for November 3. In the lead-up, primary elections will be held across states to select party candidates. The outcome of these elections will serve as a key indicator of the future direction of the Trump administration, which has deeply polarized domestic politics and influenced global dynamics. The results are likely to have significant implications for the trajectory of climate policy in the United States and internationally.

10. COP31 (Nov 9–20)

The 31st Conference of the Parties to the United Nations Framework Convention on Climate Change (COP31) will be held in Antalya, Türkiye. While Türkiye will serve as host country, Australia—also a contender to host—will take on the role of negotiation lead. Amid rising geopolitical risks, including conflicts, resource competition, and trade tensions, the urgency of climate change continues to intensify, with profound impacts on ecosystems, human lives, and the rights of future generations. COP31 will be a critical and challenging forum, requiring careful diplomacy to advance international cooperation and deliver meaningful progress.